The NSW Auditor General’s report into Local Government has again named Central Coast Council as being high risk for its financial reporting.

In a report made public on June 13, Central Coast Council was high risk in two areas including a prior year error, and its initial valuation for assets had to be corrected.

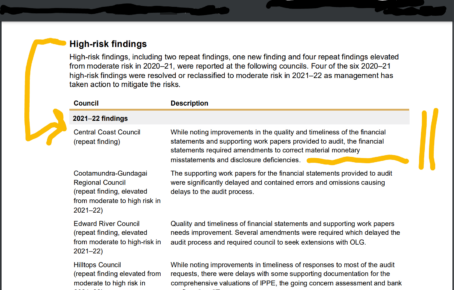

“While noting improvements in the quality and timeliness of the financial statements and supporting work papers provided to audit, the financial statements required amendments to correct material monetary misstatements and disclosure deficiencies,” the auditor general’s report stated.

A prior period financial statement error is an error identified in the current year that relates to the previous year’s audited financial statements.

The Auditor General said the Central Coast Council was one of five councils that had errors greater than $50M.

“Council’s comprehensive valuation of Community Recreation Services (open space) assets, and reconciliation between technical and fixed asset registers identified assets controlled by the council that had not been recognised in the financial statements amounting to $43.6 million,” the report stated.

“Council’s updated revaluation process for 2020–21 and internal reconciliation between the technical and fixed asset registers, identified corrections to the valuation of roads, drainage, water and sewer assets amounting to $102 million.”

A third area noted was in asset management and this was a repeat issue for the Council.

“Council’s initial fair value assessment of Infrastructure, property, plant and equipment (IPPE) did not consider the most relevant data/indices. This resulted in material corrections to the financial statements,” the report stated.

The LG Act requires councils to submit their audited financial reports to OLG by the statutory deadline of 31 October or apply for an extension.

Council was granted an extension and the finances were eventually given a tick of approval in February of this year.

The report noted that the previous qualified opinion on Central Coast Council’s 2020–21 financial statements were removed in the 2021-22 statements.

“In 2021–22 Central Coast Council addressed the issues that led to a qualified audit opinion in 2020–21 by having sufficient evidence to support the completeness and accuracy of the opening asset balances that were subject to audit qualification,” the report stated.

“ A qualified audit opinion was issued for the Central Coast Council’s 30 June 2021 financial statements because council was unable to provide sufficient appropriate evidence to support the carrying value of $5.5 billion of roads, bridges, footpaths, bulk earthworks, stormwater drainage, water supply and sewerage network assets.

“Council had been unable to reconcile the asset data (technical asset register) used to value these assets to its financial records (fixed asset register) prior to the valuation.

“Council addressed these issues in 2021–22 by performing a reconciliation of its 30 June 2021 technical asset register to its fixed asset register (pre-2021 valuation) and obtained an updated independent valuation of its roads, bridges, footpaths, bulk earthworks, stormwater drainage, water supply and sewerage network assets at 30 June 2021.”