Wants to keep the rate hike due to expire in 2031

Council-under-administration has flagged a growing gap between recurring income and expenditure.

In its long term financial plan, which estimates the growth in income and expenditure for the next ten years, a deficit kicks in in 2026-27.

The size of the deficit changes depending on four scenarios.

But the one scenario that Council recommends Administrator Rik Hart adopts at the November 28 meeting includes retaining the one-off rate increase of 15 per cent from 2021-22 that is due to expire in 2031.

This would involve another Independent Pricing and Regulatory Tribunal (IPART) determination.

“Whilst the temporary Special Rate Variation (SRV) has enabled Council’s financial recovery, the SRV was approved within the context of financial recovery, rather than being based on an analysis of financial settings required to achieve financial sustainability,” Council says.

“It is further noted that upon its expiry in 2031 Council’s revenue will drop significantly and to a point where minimum service levels will not be able to be sustained.”

Stable but not sustainable

Council says that it is financially stable due to the successful financial recovery plan, put in place in October 2020, but that like most councils in NSW, Council now needs to review its financial settings to ensure it can remain financially sustainable over the long-term.

It says significant productivity improvements have already been implemented and processes are continually reviewed but current financial settings will need more significant adjustments to secure ongoing financial sustainability.

As just one example of increasing pressures, it says cost shifting from the State Government costs Council about $45M per year.

“Examples of cost shifting include contributions to the NSW Fire and Rescue, NSW Rural Fire Services and NSW State Emergency Service, lack of adequate funding for public libraries and the failure to fully reimburse councils for mandatory pensioner rebates,” Council says.

The long term financial plan details ways of cutting costs.

These include investigating the divestment of discretionary and business activities that are not generating a benefit, financial or otherwise to the wider community.

The plan also talks about “recycling assets”.

“Through the review of Asset Management Plans and Asset Management Strategy, Council is likely to be presented with opportunities to recycle under-utilised assets (e.g., buildings and land) to obtain better utilisation and improve overall sustainability by reducing the cost of under-utilised assets and achieving commercial returns through asset recycling,” Council says.

Council sold more than $60M assets during the financial recovery.

It still has the former Gosford Council building on its list of assets and is hoping to sell that to the State Government as part of the TAFE precinct – a plan announced by the former State Government but with no deal yet finalised.

Here are the four scenarios.

# Scenario One

Scenario one is business as usual and the report, to be tabled at the November 28 meeting, says this is not an option as Council would not be able to continue to deliver services and works to the community.

It would see:

1/ Stormwater drainage service charges ceasing on 30 June 2026 due to an IPART ruling that said the charge needs to be moved from the water and sewer business to the general fund.

But to move it to the general fund, Council has to apply for a special rate variation (SRV) – which it can do.

If approved, it would simply move the charge from the water rates bill to the ordinary rates bill.

Forecasted reduction in annual service charges of $23.3M in 2026-27 if the move is not allowed.

Council Watch can’t see why IPART would not allow the charge to continue.

It said in its 2021-22 determination that it should be moved to the ordinary rates as all ratepayers benefit from the charge.

But the process is time-consuming and costly and, as CEO David Farmer said last week, SRVs are not welcomed by the community.

2/ Removal of $29.6M in 2031-32 reflecting the expiry of the SRV implemented in 2021-22.

This was the one off 15 per cent rate increase IPART allowed Council to dig itself out of its financial crisis.

At the time, Administrator Rik Hart, in his capacity as acting CEO, said it was needed to finance the repayment of the $150M in emergency loans the council acquired in December 2020.

The council is preparing to pay off $100m at the end of this year.

IPART determined the increase should stay for three years in its first determination but Council went back and successfully argued it needed the increase to stay for ten years.

Now it says it’s needed for longer.

:

:

# Scenario Two

Scenario two is based on Scenario 1 with the following additions:

1/ an extra $1M in operating revenue, indexed each year

2/ productivity target of 0.75% for materials and services every year resulting in a reduction in materials and services of $1.1M from 2024-25.

This scenario still gives the council a deficit in 2026-27 but it would be smaller.

But council says its not an option for the same reasons as option one: It would not be able to continue to deliver services and works to the community.

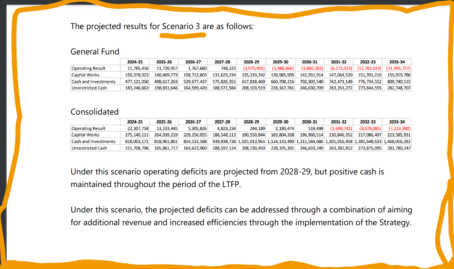

# Scenario Three

The third scenario builds in the savings from scenario two but doesn’t lose the two incomes outlined in scenario one.

For residents that means no change in the drainage charge: it would simply move from one bill to another; and the one off 15 per cent increase to their rates would not be removed, so still no change in current payments – except that each year rates generally increase with an IPART determination on how much that increase will be.

Earlier this month IPART announced a 4.8 per cent maximum rate hike for the Central Coast Council next financial year.

This has to be ratified by Administrator Rik Hart at a future meeting.

The deficits would still kick in in 2026-27 but the underlying cash position would not go into the negative if a combination of the additional revenue and increased efficiencies are implemented.

# Scenario Four

Under Scenario four, Council would keep the rates increases from scenario three.

It would spend an extra $10M on maintenance.

“Under this scenario operating deficits are projected earlier than in Scenario 3 due to the increased asset maintenance expenditure,” Council says.

“Like Scenario 3, under this scenario projected deficits can be addressed through a combination of aiming for additional revenue and increased efficiencies through the implementation of the Strategy,” Council says.

“Service levels could also be reviewed, and priorities established in consultation with the community.

“However, the magnitude of the projected operating deficits and the associated timing will require the required actions to commence as soon as possible.’’

Council said it would use Scenario 3 as the basis for the 2024-25 Operational Plan and Budget.

But it would like to build capacity so in later years it can increase its investment in asset maintenance as shown in Scenario 4.

Administrator Hart will address the issue at the November 28 meeting.